March 25, 2015 by Justin La Plante

I recently read Larry Kaufmann’s, The Politics of Ridesharing in the Isthmus. As a former cab driver in Madison, I take issue with many errors in his article.

Graphic: David Michael Miller, The Isthmus

Using the Uber app for payments

Firstly, Kaufmann claims that no money is changing hands between the passenger and driver using the Uber service. This deceptive talking point is often used by Uber’s own representatives to disguise the fraudulent nature of how Uber really does business.

While paper cash is not used in the transaction, money is being transferred directly from the customer’s debit or credit card account by way of the Uber app. The app requires a connected account before services can be provided. The funds from payments are then split at a rate of 80% for the driver and 20% for Uber. This method of charging funds limits a customer’s choice of payment method and automatically discriminates against those who are unable to use a credit or bank card, as well as those who don’t have a smart phone capable of running the Uber app. Uber drivers are also entirely cut out of the process of tipping.

Wait times with Uber and discrimination

Kaufmann claims that wait times for the Uber service are lower than those of traditional cab services. While he is right about the wait times, he fails to examine exactly why Uber drivers get to their preferred stock of customers so quickly.

Screen captures of the Uber app activity in Madison show that Uber is servicing barely 20% of the city’s geographic area. While other cab companies operate throughout Madison, Uber makes it clear that they will consistently deny and avoid orders for service in areas they deem too “poor” or “off-color.” Add to this the number of customers already denied service for being too poor to own a smart phone or to old or inexperienced to use one.

Screen captures of the Uber app activity in Madison show that Uber is servicing barely 20% of the city’s geographic area. While other cab companies operate throughout Madison, Uber makes it clear that they will consistently deny and avoid orders for service in areas they deem too “poor” or “off-color.” Add to this the number of customers already denied service for being too poor to own a smart phone or to old or inexperienced to use one.

Uber relies on the reviews of those who use smart phones regularly. That makes up a good amount of UW students and the affluent of the Isthmus area. As you can see from this list of regular screen captures taken from September to December of 2014 on the Ride Safe Madison website, Uber maintains a consistent denial that the majority of Madisonians even exist.

Uber’s fare rates and fraudulent charges

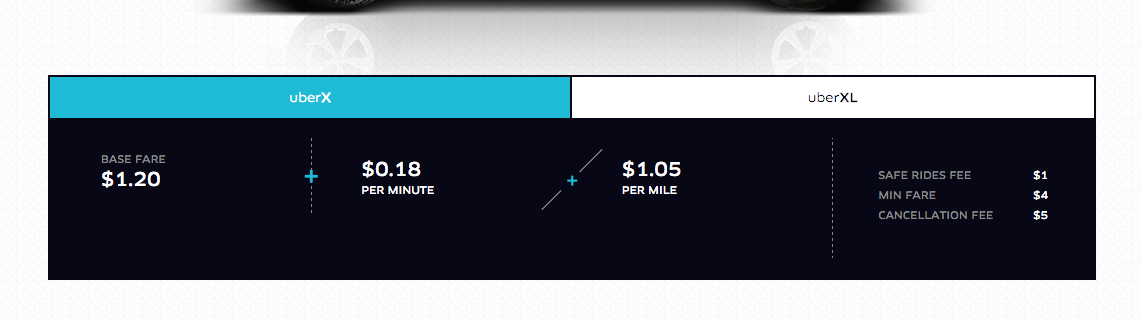

Kaufmann claims that Uber’s fare rates are lower than that of traditional cab companies in Madison. That claim is only 50% true. While Uber’s current rates (dropped by $2 per fare in November of 2014) are cheaper than that of Madison Taxi or Union Cab, the average rates charged by Green Cab and Badger Cab are still $2 to $3 cheaper per fare than Uber.

Surge pricing

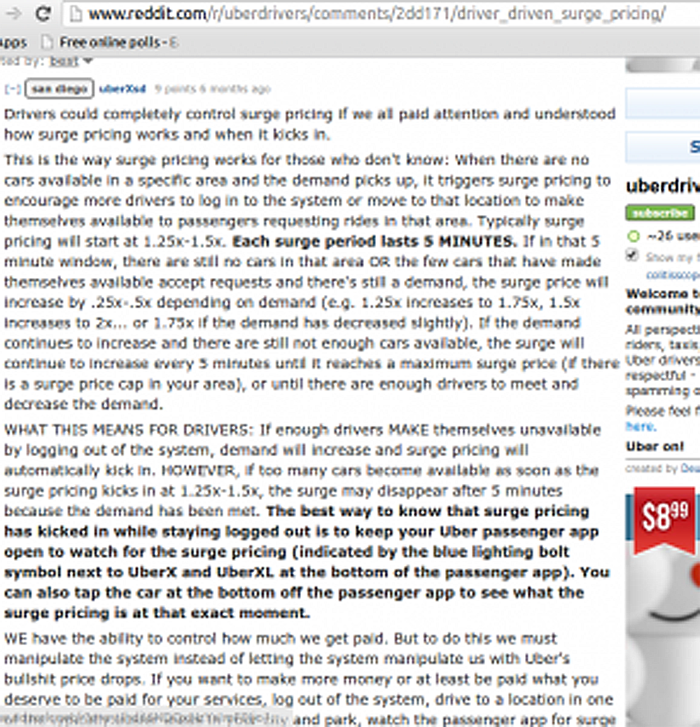

A recent post on Uber’s Reddit page detailing how Uber and their drivers manipulate surge pricing.

Uber regularly practices a system of over charging that they call “surge pricing,” which has already charged some Madisonians as much as $80 to go from Camp Randal to East Washington near East town Mall. Uber claims that surge pricing meets the needs of supply and demand during times of increased traffic and orders. However, app activity during surge priced times from the same list of screen captures show Uber is only activating the higher surge prices in specific geographic areas and then deactivating surge pricing after a few of their drivers have gotten fares at the higher rates. Meanwhile the majority of the city’s geographic area not in the surge price areas go entirely without service while Uber drivers avoid them.

Why would anyone pick up customers that would pay them only $5 when they can pick up customers who will pay them $25 for the same amount of time and distance? This system is not being used as a means of meeting supply and demand, but more to discriminate against lower-income residents while cherry picking the market to favor higher profits.

The Safe Rides Fee and bogus insurance

Another additional $1 fee that is charged to the customer and the portion of the driver’s cut of payments are what Uber claims as a “Safe Rides Fee.”

Uber claims that the Safe Rides Fee is “a fee added to UberX fares on behalf of drivers (who may pay this fee to Uber) in cities with UberX ridesharing. This Safe Rides Fee supports continued efforts to ensure the safest possible platform for Uber riders and drivers, including a federal, state, and local background check process, regular motor vehicle checks, driver safety education, development of safety features in the app, and more. For complete pricing transparency, you’ll see this as a separate line item on every UberX receipt.”

Uber claims that the Safe Rides Fee is “a fee added to UberX fares on behalf of drivers (who may pay this fee to Uber) in cities with UberX ridesharing. This Safe Rides Fee supports continued efforts to ensure the safest possible platform for Uber riders and drivers, including a federal, state, and local background check process, regular motor vehicle checks, driver safety education, development of safety features in the app, and more. For complete pricing transparency, you’ll see this as a separate line item on every UberX receipt.”

Why Uber charges this fee as a part of the service concerning the driver’s training, background check and checks of their vehicles is confusing. Uber performs no driver training beyond a series of short videos with no review or testing process, virtually no in-person vehicle inspections (Madison Uber drivers only send in pictures of their vehicles), and their background check process has already overlooked registered sex offenders. Convicted felons were allowed to drive on the UberX platform, the very service on which Uber charges the Safe Rides Fee. UberX is the only Uber service offered in Madison.

It is even more confusing when you look at the insurance coverage Uber claims it provides for its passengers and drivers during rides. This insurance coverage has not turned up to compensate those injured and even killed by Uber drivers, even when those people were customers.

Since Uber does not require their drivers to maintain a commercial insurance policy to use the service, it is then left to Uber’s advertised insurance policy to be in place.

Section 5 of Uber’s own TOS clearly states that Uber maintains no liability for claims, damage or injuries suffered by those using the service. Uber’s current service term agreement section 5 from www.uber.com/legal:

5. DISCLAIMERS; LIMITATION OF LIABILITY; INDEMNITY

DISCLAIMER.

THE SERVICES ARE PROVIDED “AS IS” AND “AS AVAILABLE.” IN ADDITION, UBER MAKES NO REPRESENTATION, WARRANTY, OR GUARANTEE REGARDING THE RELIABILITY, TIMELINESS, QUALITY, SUITABILITY, OR AVAILABILITY OF THE SERVICES OR ANY GOODS OR SERVICES OBTAINED THROUGH THE USE OF THE SERVICES, OR THAT THE SERVICES WILL BE UNINTERRUPTED OR ERROR-FREE. YOU AGREE THAT THE ENTIRE RISK ARISING OUT OF YOUR USE OF THE SERVICES, AND ANY THIRD PARTY GOOD OR SERVICES OBTAINED IN CONNECTION THEREWITH, REMAINS SOLELY WITH YOU, TO THE MAXIMUM EXTENT PERMITTED BY APPLICABLE LAW.

THIS DISCLAIMER DOES NOT ALTER YOUR RIGHTS AS A CONSUMER TO THE EXTENT NOT PERMITTED UNDER THE LAW IN THE JURISDICTION OF YOUR PLACE OF RESIDENCE.

LIMITATION OF LIABILITY.

UBER SHALL NOT BE LIABLE TO YOU FOR INDIRECT, INCIDENTAL, SPECIAL, EXEMPLARY, PUNITIVE, OR CONSEQUENTIAL DAMAGES, INCLUDING LOST PROFITS, LOST DATA, PERSONAL INJURY, OR PROPERTY DAMAGE, EVEN IF UBER HAS BEEN ADVISED OF THE POSSIBILITY OF SUCH DAMAGES. UBER SHALL NOT BE LIABLE FOR ANY DAMAGES, LIABILITY OR LOSSES INCURRED BY YOU ARISING OUT OF: (i) YOUR USE OF OR RELIANCE ON THE SERVICES OR YOUR INABILITY TO ACCESS OR USE THE SERVICES; OR (ii) ANY TRANSACTION OR RELATIONSHIP BETWEEN YOU AND ANY THIRD PARTY PROVIDER, EVEN IF UBER HAS BEEN ADVISED OF THE POSSIBILITY OF SUCH DAMAGES. UBER SHALL NOT BE LIABLE FOR DELAY OR FAILURE IN PERFORMANCE RESULTING FROM CAUSES BEYOND UBER’S REASONABLE CONTROL. YOU ACKNOWLEDGE THAT THIRD PARTY TRANSPORTATION PROVIDERS PROVIDING TRANSPORTATION SERVICES REQUESTED THROUGH UBERX MAY OFFER RIDESHARING OR PEER-TO-PEER TRANSPORTATION SERVICES AND MAY NOT BE PROFESSIONALLY LICENSED OR PERMITTED. IN NO EVENT SHALL UBER’S TOTAL LIABILITY TO YOU IN CONNECTION WITH THE SERVICES FOR ALL DAMAGES, LOSSES AND CAUSES OF ACTION EXCEED FIVE HUNDRED U.S. DOLLARS (US $500).

THESE LIMITATIONS DO NOT PURPORT TO LIMIT LIABILITY THAT CANNOT BE EXCLUDED UNDER THE LAW IN THE JURISDICTION OF YOUR PLACE OF RESIDENCE.

The other portion of the same document that is in all caps requires the passenger to agree that Uber isn’t even providing them with transportation services and has no liability with respect to any claims for how safe or reliable the service may or may not be.

In simple legal terms, this means that what Uber advertises as “safety” and “insurance” are instantly invalidated as soon as an Uber driver or customer switch on the app and hit the “agree” button.

Paul Soglin and Scott Resnick on Uber

Kaufmann’s opening comparatives on the political divide over Uber and other transportation network companies (TNC) between incumbent Paul Soglin and his mayoral challenger Scott Resnick produced a rather funny foot-in-mouth irony.

Kaufmann states:

Leading the charge is Mayor Paul Soglin, who treats Uber as if it were the spawn of Satan, or at least the Koch brothers.

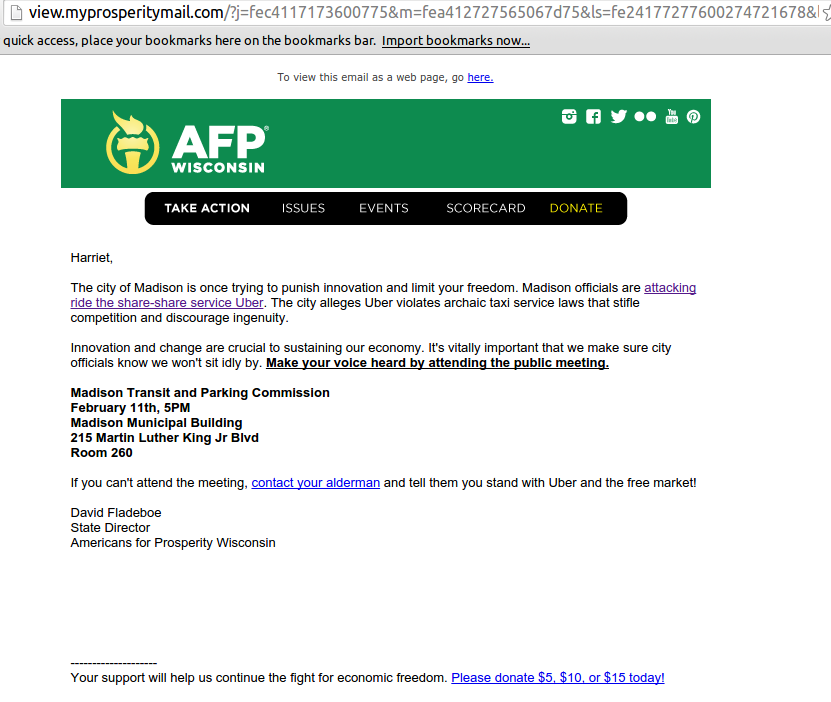

Shortly before a recent city Transportation and Parking Commission (TPC) council meeting, the Koch Brothers lobbying front AFP threw its hat in to support Uber with this email urging Madison residents to show up at a TPC council meeting and send emails to the city council in support of Uber’s efforts to do business in Madison.

Shortly before a recent city Transportation and Parking Commission (TPC) council meeting, the Koch Brothers lobbying front AFP threw its hat in to support Uber with this email urging Madison residents to show up at a TPC council meeting and send emails to the city council in support of Uber’s efforts to do business in Madison.

Scott Resnick has since religiously avoided questions concerning the Koch Brothers involvement and support of Uber. Though Resnick had been attending TPC meetings in support of his own revisions to the city’s transportation ordinance, he skipped this meeting entirely. Paul Soglin did not. As a former cab driver himself, Soglin understands how taxis and peer-to-peer/point-to-point commercial transportation works and how it can be manipulated to favor certain customers over others.

Scott Resnick claims that companies like Uber, Lyft and other TNCs are here to stay. This is a regular byline of officials in cities that have given in to the massive deregulation and the discriminatory business model that companies like Uber bring to the table.

Both Soglin and Resnick have made proposals for changes to the city’s current transportation ordinances which would allow Uber to operate here while more or less adhering to basic rules of proper insurance and safety requirements. However, while Soglin’s proposals would require things like proper background checks and insurance coverage on the part of Uber and Uber drivers, Resnick’s proposals are a kind of “soft regulation” that Uber knows it could manipulate. With Resnick’s proposals, they could operate without full compliance, as they have done in several US cities that claim responsible allowances have been made for Uber and other TNCs.

A recent ordinance change in Milwaukee claimed to allow Uber to operate legally there. While Uber announced that their operations in Milwaukee were now legal, they have not fully complied with the vehicle inspections mandated by the Milwaukee ordinance, along with other key elements of the law.

Kaufmann claims that ordinances mandating insurance and safety would be unnecessary when applied to Uber because he claims the company:

… is a well-capitalized firm that can absorb potential liability from accidents.

However, there is currently not one US city or state that has not reported major problems with ordinance compliance from Uber after passing allowances for the company to operate. Uber has yet to pay compensation or even claim ethical liability for several injuries and two deaths caused by Uber drivers in the last year alone.

For all its claimed billions and from its own contracting, Uber has no interest in maintaining liability with respect to its own business. Unlike Kaufmann and Resnick, Paul Soglin knows this and has been trying desperately to end the madness of the so-called “sharing economy” before it takes root in Madison.

Kaufmann talks about reliability with the Uber service. And yet Uber is not mounting cameras in their vehicles to maintain that claim of reliability as companies like Green Cab do. There would be no need for speculative claims or a rating system when one can see and hear what transpires in and outside the vehicle.

Kaufmann’s Fake Facts

Kaufmann wraps this article with more of the economics and popularity of the “shared economy.” Mentioning companies like AirbnB, citing examples of the statistical popularity of Uber with “tech-savvy” students and the “millennial” generation, and a speculation that every Epic employee in the last ten years must also love Uber is entirely unsubstantiated. He again fails to be responsible about the facts behind these claims. He is talking about the the rich and tech-savvy young that Uber has easily exploited with social network manipulation, false advertising and lies. That is hardly a large or even remotely diverse cross-section of Madison or anywhere else for that matter.

Meanwhile, those who can read and understand a TOS agreement before hitting the “agree” button, are consistently denied service from companies like Uber for being too old, poor or non-white, and who would prefer to pay for a ride with a service that actually has insurance are not impressed. There are plenty who use Uber and talk about it online, but they are hardly the vox populi or even a remotely well-informed portion of society.

Kaufmann’s “credentials”

While Kaufmann claims to be an “economic consultant,” there is little that would support that. The Heartland Institute, the fake non-profit and lobbying firm which calls itself a “think tank,” notes Kaufmann as an “expert.” It is not surprising that the Heartland Institute has a close personal history with The Koch Brothers and AFP. It is clear what Kaufmann’s intentions were with his “article.”

The real economics of Uber and the Sharing economy

Any legitimate economist with the least bit of ethics understands the kind of economic disaster that Uber represents. The company holds the majority of its assets in a fleet of drivers nationwide who are using their personal vehicles as a means of providing commercial transportation without proper notifications or arrangements with lease, warranty, service or their own insurance policies. They are providing those services under an insurance policy which Uber invalidates with its own contracting. This makes Uber’s incidental costs an exponentially growing behemoth that inevitably end up coming out of the pockets of taxpayers and insurance policy holders.

Those who tout Uber as some wonderful new idea forget that many large companies in the US once did business virtually identical to the business model that the shared economy proposes: before the great depression.

Every month we read about insurance, safety and ordinance violations committed by Uber. Communities that deal with the company have lost money and continue to suffer because Uber refuses to live up to its own claims or respect simple laws that would ensure their drivers and customers are not being defrauded or themselves defrauding others.

The idea of peer-to-peer ride share apps is not inherently fraudulent by nature. Already each of Madison’s local cab companies has either developed or is developing their own connection and ordering apps. Some cab companies and app development companies have even proposed creating a means to allow independent drivers the ability to operate as ride share vehicles without limiting how a customers pays, inviting discrimination and surge pricing, or operating without any real insurance.

But what Uber has done is to take a good idea and use it in the worst way possible.

That is not innovation, that is a confidence scam.

Leave a comment